Can Shopping For Small Business Health Insurance Be Easy & Fun?

“This post was sponsored by UnitedHealthcare. All thoughts and opinions are my own.”

Shopping For Small Business Health Insurance

A little over a month ago, we published the first part of this series. It was titled “The Simple UnitedHealthcare Small Business Solution”. It was an overview of the benefits to small businesses of providing a healthcare benefit to their employees. In this follow-up, I will loosely walk through the process to show just how easy it is.

The entire 3-part sign-up process can take as little as 20 minutes. So if your company has between 2 and 50 employees (including you), read on….

You will be given options to create an ID and save your progress. But you will know your full costs and those to your employees before you must take this step.

So by all means, ‘take a test drive’ before making any decisions.

(Note: If you’re a two-person company but share a single healthcare policy, then, unfortunately, this tool will not work for you. It requires businesses with at least two people with 2 separate health policies)

Here are the 3 sections within the tool, which we’ll get to in turn, below:

- Medical Plans

- Employee Details

- Monthly Budget

I was going to walk everyone through the various screens. But this tool is so very easy and intuitive; I promise you won’t need a tutorial. So instead, here is a brief description of what you can expect to find…..

Medical Plans

At the time of writing, this service is not available in every State. However, to repeat my praise of UHC from the previous article: wherever you are, you’re likely to find their plans are priced highly competitively, with wide-ranging plans. So if you can’t do it online, give them a call.

Here are the States where this online tool is available: CA, AR, TN, MI, MD, VA, WV, IN, KY, PA, OH, NC, WI, IL, FL, GA, WA.

To kick off your tour, click this link: https://smallbusiness.uhc.com/

It’s in this section that you:

It’s in this section that you:

- Enter your zip code

- Select the number of employees

- Decide when you want coverage to start

The possible start dates shown are all either the 1st or the 15th of a month. But you don’t have to select any of the dates shown.

Just know that whatever you select here, you can change later. So there’s no need to feel that your answer must be perfect. And if you need help with anything, help is always just a call or an email away.

This section is easily larger than the other two combined

Your Plan Selection

This is the fun part!

I hope you’ll be as pleasantly surprised as I was. I know that when I checked into business health insurance for myself, a couple of years ago, the numbers were WAY higher than the 17 plans that were returned to me when I did my walk-through.

The range of plans I received were presented in 3 sections:

- High Deductible

- These have no co-pay for visits, and the deductible is also the max out-of-pocket expense for the year

- Moderate Deductible

- Slightly higher premium; much lower deductible, and a slightly lower maximum out of pocket expense

- Low Deductible

- Again, slightly higher premiums, in return for lower co-pays and lower maximum out of pocket. And zero deductible!

The numbers you see will include your presumed contribution and how much this means that your employees will have to pay.

This number is not final!

You can change further into the process. You will note though, that your contribution remains the same for each plan. So your employee’s portion varies based upon their choice.

You have the choice to remove any of the plans you wish, and not pass them on for your employees to see. Just know though, that if you provide your employees with the choice of at least 6 plans, they will have access to a helpful tool – the ‘Employee Fit Finder’ – when it’s their time to decide their plan choice.

The ‘Employee Fit Finder tool’ is:

“an interactive tool that helps employees narrow their plan choice by asking them questions about their family and lifestyle”

It’s also on this page that you can see the Dental and Vision plans that will be offered to your employees. This needn’t cost you anything extra, but that decision can wait. (That’s one of the things you can discuss with your adviser.)

Employee Profiles

More importantly for now, below the section on Dental and Vision plans, you will see this:

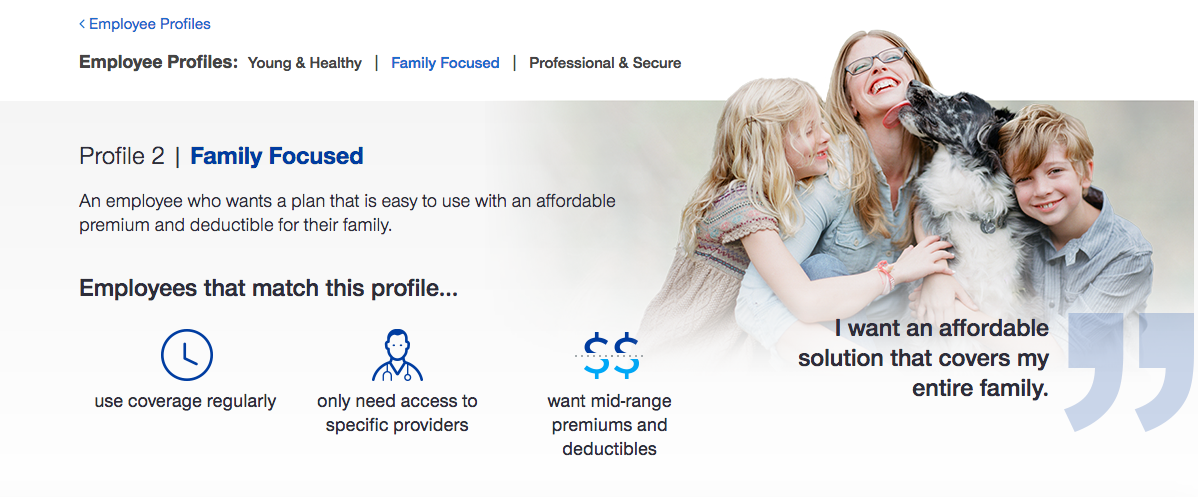

If you click there, you will see three common profiles:

If you click there, you will see three common profiles:

- Young and Healthy

- Family-focused

- Professional and Secure

Each enables you to view the varying needs.

This is what the family-focused page looks like:

Scroll down the page a little, and you’ll see the plans suggested for this profile

Scroll down the page a little, and you’ll see the plans suggested for this profile

You don’t have to look at the profiles. But they’re there if you want to. It could help you decide on whether or not to keep a particular plan in the package you offer, if you were considering removing any. You can do this further into the process. And this feature gets more helpful later, as you will see….

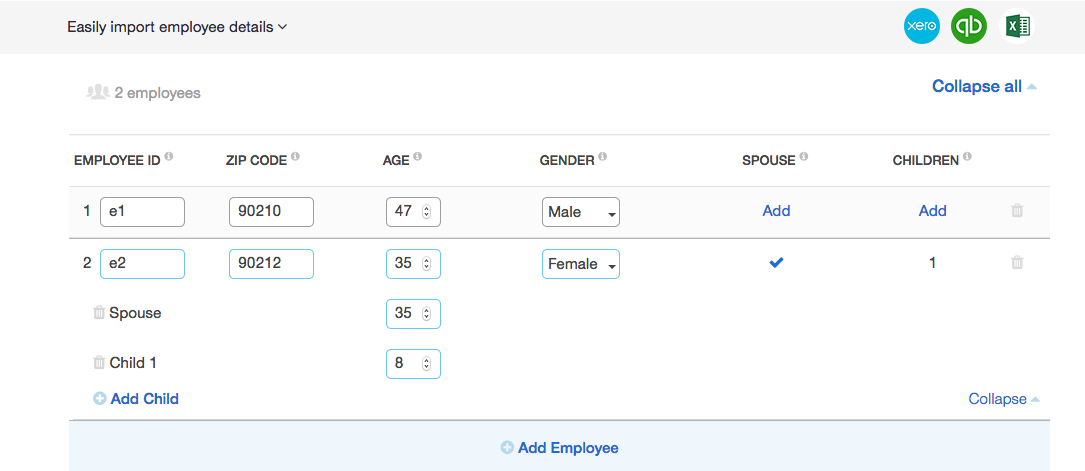

Employee Details

It here that you enter or import your employee details: Employee initials (or other identifier), ZIP Code, Age, Gender, & option to add spouses and children.

Remember, you want a plan also, so be sure to enter your own details!

Did you notice “Easily Import Employee Details” toward the top left of the page? If you click on the down arrow, you’ll be given options to import details from Xero, QuickBooks and Excel. Depending on how many employees you have, you may wish to utilize this option.

Did you notice “Easily Import Employee Details” toward the top left of the page? If you click on the down arrow, you’ll be given options to import details from Xero, QuickBooks and Excel. Depending on how many employees you have, you may wish to utilize this option.

Once you’ve entered all of your details, scroll down to the bottom of the page. If you “Explore employee profile” now, any of your employees who match the profile you select, will show up here.

When you click “Continue” here, you’ll be invited to create a profile and save your details here. Do so if you wish. But if you’d prefer to see a little more, just click “No. thanks”.

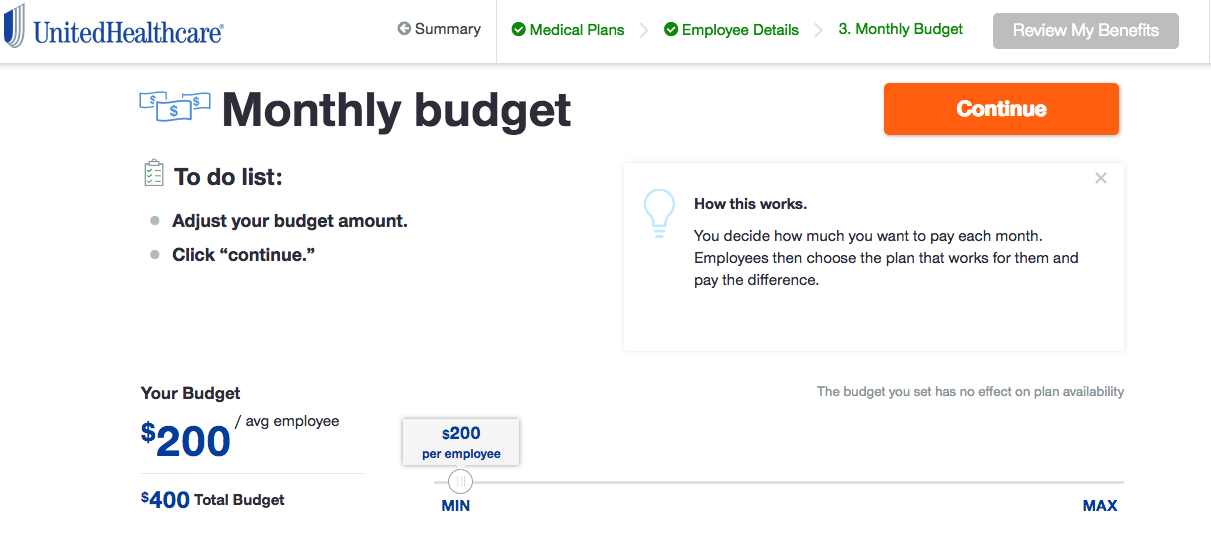

Monthly Budget

You’re almost done!

The screen you will now see is in two parts.

On top, there’s the costs breakdown of the entire plan. This includes all employees:

- The total monthly cost range (you + your employees).

- Your employer contribution (this is fixed, no matter what your employees choose)

- The total employee cost range (we don’t know what they will pick, but the numbers shown are their minimum and maximum contributions).

On the second half of the screen, the cost range for each employee appears.

This shows your contribution to their policy, plus the complete range from low to high that each employee may pay.

Note: You probably already know this, but your employee contributions are typically taken through payroll deductions, and are removed pre-tax. Therefore, their taxable earnings are reduced by the cost of the policy they choose. So their net out-of-pocket costs will be reduced by however much tax they save. Obviously, this depends on their tax bracket and any local taxes, so there’s no way of giving a percentage here.

It’s here that you get to decide the average amount you want to contribute to each employee’s plan. Either enter a number or use the interactive slider tool. As stated, it is an average amount, so each person may not get exactly the same.

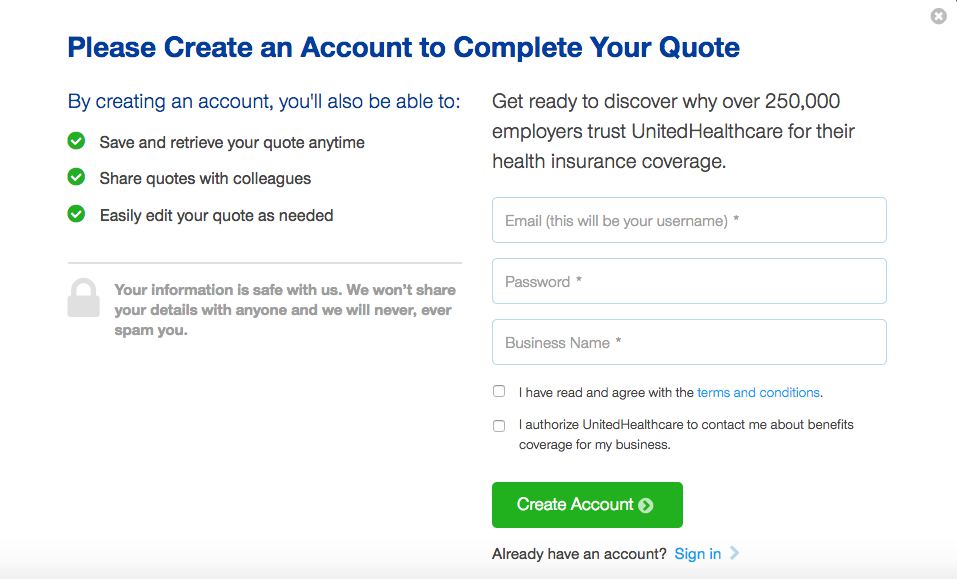

You’ve completed the online portion. Presuming you’re happy with what you saw, now’s the time to sign up if you don’t want to lose what you entered. However, also by now, you’re aware that this really is very easy, so you determine if you’d rather leave and come back another day. If you sign up, there are, of course, no obligations.

You’ve completed the online portion. Presuming you’re happy with what you saw, now’s the time to sign up if you don’t want to lose what you entered. However, also by now, you’re aware that this really is very easy, so you determine if you’d rather leave and come back another day. If you sign up, there are, of course, no obligations.

After you have signed up

After you have signed up

Confession time. I did not sign up. However, our trusted and wonderful researcher did. And this is what she found….

After reviewing your plans, you can download your completed proposal as a .pdf and share a link with your employees and other business team members.

Once you have confirmed your benefits, you can then provide your contact and business information.

After that, payment options are made available along with a final review of your plan coverage.

Then, in UHC’s own words:

“A coverage advisor will make sure you are set up in UnitedHealthcare’s systems and help you with adding specialty benefits to your coverage.”

In Closing

We hope this has been helpful to you. If you have any questions, please leave a comment below, and we’ll seek out the answer for you if we don’t already know it.

Blog disclaimer required by the FTC

The views expressed do not reflect those of UnitedHealthcare nor its affiliates. They are the personal opinions of the authors. While UnitedHealthcare has made every attempt to ensure accuracy, the information contained in these blogs may change and UnitedHealthcare assumes no responsibility for errors, omissions, contrary interpretations of the subject matter or information herein or for any losses, injuries, or damages arising from its display or use. These blogs may connect to other websites maintained by third parties over whom UnitedHealthcare has no control. UnitedHealthcare makes no representations as to accuracy, completeness, suitability, or validity of any information contained in those linked blogs or third party websites. Blogs are for general informational purposes only and not intended to be medical advice or a substitute for professional health care.

Featured image: Copyright: ‘https://www.123rf.com/profile_maridav‘ / 123RF Stock Photo

Andy Capaloff

Latest posts by Andy Capaloff (see all)

- The Art of Asking Questions [Interactive] - October 17, 2023

- The Metaverse Is Not Dead. It’s Resting! - September 6, 2023

- How Can You Hire For Jobs That Nobody Has Experience In? Aptitude! - June 13, 2023